Crypto lender Celsius declares Chapter 11 bankruptcy in New York

Quick Take

- Crypto lender Celsius has filed for Chapter 11 bankruptcy, according to court filings.

- In a statement, Celsius said it had $167 million in cash “to support certain operations during the restructuring process.”

Crypto lender Celsius has declared Chapter 11 bankruptcy, court filings show.

The firm declared assets between $1 billion and $10 billion, with an equal amount in estimated liabilities, according to the Chapter 11 petition.

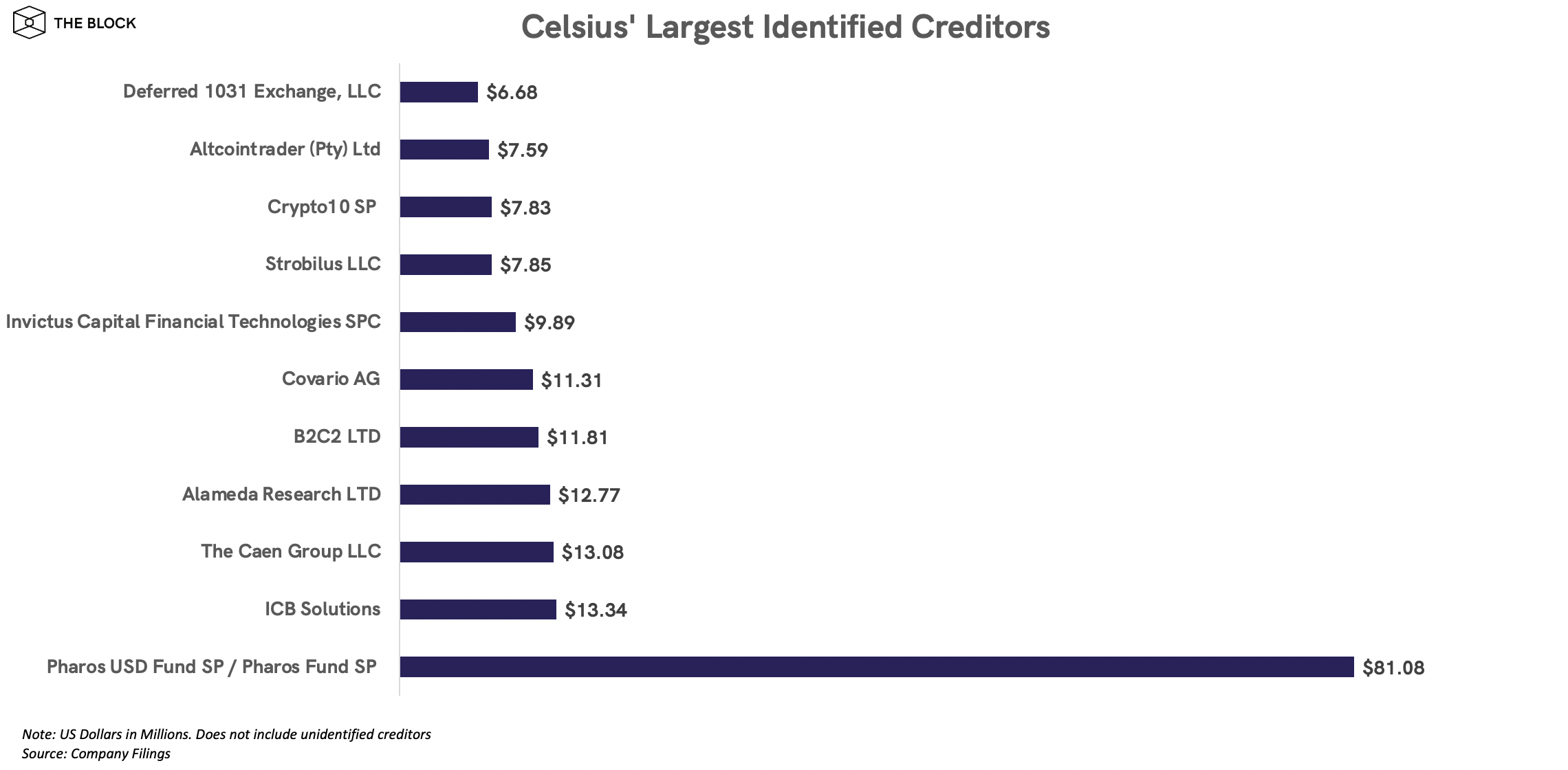

Celsius claimed more than 100,000 creditors in its petition. The petition names Pharos USD Fund SP and Pharos Fund SP as its largest unsecured creditor, with an unsecured claim of approximately $81 million. Other named creditors include ICB Solutions, The Caen Group LLC, Alameda Research, B2C2, and Covario AG, among others.

In a statement, Celsius said it "has $167 million in cash on hand, which will provide ample liquidity to support certain operations during the restructuring process."

The firm is being represented by Kirkland & Ellis LLP, per the petition. A total of eight Celsius-related entities are declaring bankruptcy.

Founded in 2017 by Alex Mashinsky and Daniel Leon, Celsius offered retail investors attractive returns on their crypto holdings under the slogan "unbank yourself." The company, which moved its headquarters from London to New Jersey last year, had grown to manage more than $10 billion in assets and claimed more than 1.7 million users.

But this year's crypto market slide left Celsius insolvent, and on June 12 it froze client withdrawals, transfers and swaps.

As The Block reported last month, Celsius's lawyers had been pushing for it to enter Chapter 11 bankruptcy for a while — while the company's executives attempted to avoid it at all costs. The firm had instead sought a show of support from app users to help win the internal argument. Amid the tension, the Wall Street Journal reported this week that Celsius had replaced its legal advisers.

Chapter 11 bankruptcy allows a company to continue operations while meeting its obligations to indebted parties. This is usually executed by proposing a plan of reorganization to be approved by creditors and overseen by a legal team.

Since halting withdrawals in June, Celsius's woes have mounted — with state regulators in the US reportedly lining up to investigate its business practices. This week, the Vermont Department of Financial Regulation said Celsius's representations about the safety of customer funds were "untrue” and accused the company of engaging in an “unregistered securities offering” by offering cryptocurrency interest accounts to retail investors.

The state of Celsius's finances has scared off potential saviors. The Block reported last month that crypto exchange giant FTX looked at making a deal with the troubled firm but ultimately walked away after finding a $2 billion hole in its balance sheet.

“This is the right decision for our community and company,” Mashinsky said in a statement. “We have a strong and experienced team in place to lead Celsius through this process. I am confident that when we look back at the history of Celsius, we will see this as a defining moment, where acting with resolve and confidence served the community and strengthened the future of the company.”

Petition by MichaelPatrickMcSweeney

This story is developing and will be updated.

© 2023 The Block. All Rights Reserved. This article is provided for informational purposes only. It is not offered or intended to be used as legal, tax, investment, financial, or other advice.